Insights & Perspectives from Financial Advisors Near You

Stay informed with timely commentary, thoughtful analysis, and real-world financial insights from the team at Cahaba Wealth Management. Our blog and podcast offer a deeper look into the trends, strategies, and market developments shaping today’s financial landscape. Whether you’re looking to better understand investment principles, navigate economic shifts, or explore planning strategies for your future, we are here to help you make more confident, informed decisions.

Financial considerations before you make the decision to retire

Cahaba Wealth Management is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by the SEC nor does it indicate that the adviser has attained a particular level of skill or ability. Cahaba Wealth Management is not engaged in the practice of law or accounting. Always consult an attorney or tax professional regarding your specific legal or tax situation. Content should not be construed as personalized investment advice. The opinions in this materials are for general information, and not intended to provide specific investment advice or recommendations for an individual. Content should not be regarded as a complete analysis of the subjects discussed. To determine which investment(s) may be appropriate for you, consult your financial advisor.

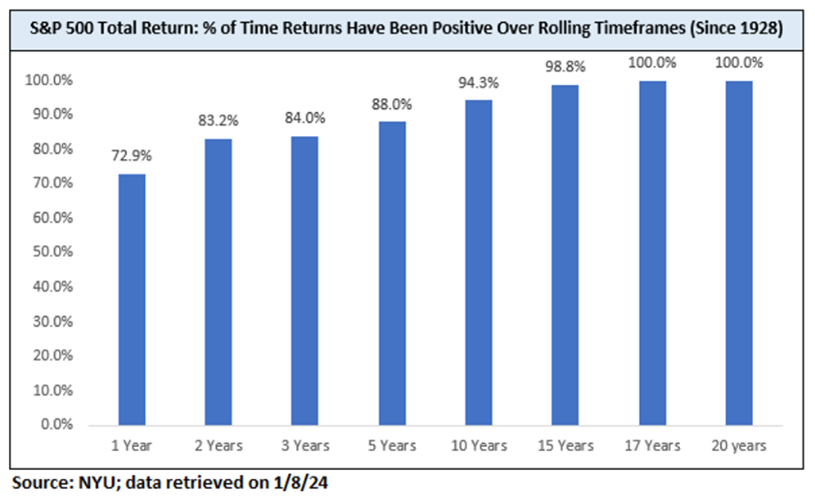

“Should I invest now (or stay invested) if the stock market is at all-time highs?” Given there are so many all-time highs in the stock market, we are asked to answer this question with shocking frequency. We know that over time the market goes up, but there tends to be more emphasis and concern about the timing of the next drop or bear market. It is enticing to think we can manage our portfolios to avoid such situations. In reality, if an investment’s time horizon was long enough, the stock market has ALWAYS provided positive returns. So, how long is “long enough”?

Since 1928, S&P 500 returns have been positive over a one-year period 73% of the time1. Not a bad percentage! If you have a ten year investment time horizon, which most of our clients do, the stock market has produced a positive return in 94% of those ten-year periods. When we extend the time horizon to twenty years, we see that returns have been positive 100% of the time. Although past performance is not indicative of future results, historical data shows that staying invested through market turbulence has always been the better decision.

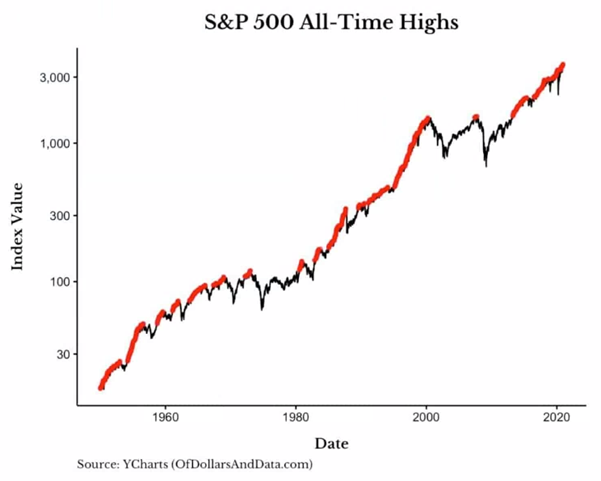

Conversely, what happens when the market is at all-time highs? Let’s first look at a chart depicting S&P 500 returns since the 1950s:

Each red instance on the accompanying chart represents days when the stock market reached an all-time high. As expected, this chart does have periods where the market did not reach its peak (i.e., returns represented by a black line), but there are more red sections than there are not. One of the most interesting components of the chart is that the red portions tend to bunch together. In other words, all-time highs have historically signaled more all-time highs. While different analysts and economists often debate the market and its parameters, the data supports this general concept in almost every case!

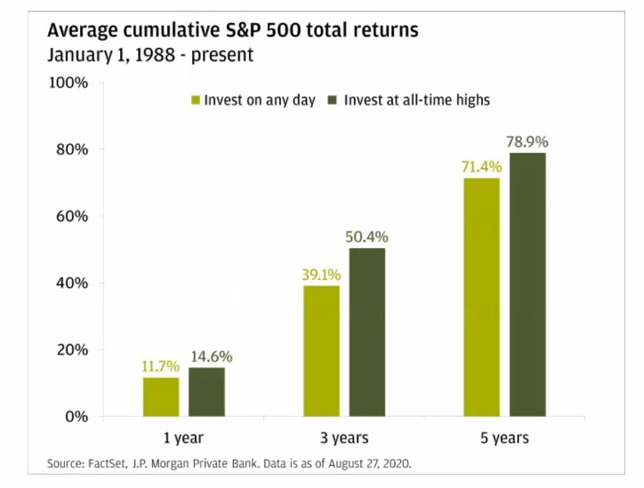

The following table pulls from a 1988-2020 dataset of market returns and supports the claim that investing during all-time highs has not been detrimental to investors. Over this time period, the average one year return in the stock market following an all-time high was 14.6%, beating the average return from investing on any given day throughout the data sample. Cumulatively, over the next five years following an all-time high in the market, an investor’s portfolio would have done materially better by investing at an all-time high as opposed to picking any other starting day at random (78.9% vs 71.4%).

The data – despite its source or time frame – generally comes to the same conclusion: one is better investing at all-time highs than they are by picking a day at random to invest. There is a consensus throughout financial research that this benefit has the greatest impact for time periods in the 1-5 year range. Said differently, as your investment horizon extends, timing takes a back seat to consistency when considering the long-term benefit. In the long run, the market goes up and investors are compensated time and time again for the risk they are taking.

By knowing your risk tolerance and your investment horizon (the time you have until you need to access your money), you can invest intelligently and improve your specific long-term outcomes. We encourage portfolio diversification and client-specific market risk exposure. This is why we prioritize knowing clients’ parameters and risk tolerances here at Cahaba Wealth.

Arguably the greatest caveat to our discussion is that no one can successfully and consistently time the market over the long run. This has been proven time and time again! Pretending to know which all-time high is the last one for the foreseeable future is nearly impossible. Stay away from this trap. Be diversified, take the appropriate amount of market risk and stay invested!

Don Keeney, CFA, CFP® is a financial advisor in the Nashville office of Cahaba Wealth Management, www.cahabawealth.com.

Cahaba Wealth Management is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by the SEC nor does it indicate that the adviser has attained a particular level of skill or ability. Cahaba Wealth Management is not engaged in the practice of law or accounting. Always consult an attorney or tax professional regarding your specific legal or tax situation. Content should not be construed as personalized investment advice. The opinions in this materials are for general information, and not intended to provide specific investment advice or recommendations for an individual. Content should not be regarded as a complete analysis of the subjects discussed. To determine which investment(s) may be appropriate for you, consult your financial advisor.

“But wouldn't you like to know

How it feels to live

Like a free man

To give

When there's nothing in your hand

Run like only the river can

Like a free man”

Angie Aparo

For many (I would suggest for all of our clients), retirement is the dream. Though I can honestly say that my career has been my avocation as well as my vocation, not everyone can state the same. They look forward to retirement, and in some ways, view it as freedom. The freedom to do what they want, when they want, in whatever way they want to do it. But let’s not pretend – retirement isn’t easy. Why is that?

My partner Chris Conkell and I discussed in our most recent podcast episode that retirement is a very recent phenomenon. 1800s farmers didn’t retire; they worked until they couldn’t work anymore. The human brain has been hard wired to hunt and gather, to provide for loved ones, and to work. Retirement, while freeing in some ways, can also present challenges to those thousands of years of wiring. What will I do every day? Can I really afford to spend my assets? Can I replace my colleagues with others who fulfill me? How did I get this “Honey Do” list?

At Cahaba Wealth Management, we spend a great deal of time working with our clients prior to retirement to help them begin to think through this. One of the hardest concepts for our clients to accept is that when they retire, they will begin to deplete those assets that they have spent a lifetime saving. This requires approaching life with an “Abundance” mindset – the belief that there are enough resources and successes to share with others.

If we believe that a client does not have enough assets and/or income streams to retire, we deliver that message with empathy. While not fun, having that conversation is part of our job and we take that responsibility seriously. There is no more important asset than a client’s ability to earn income.

A more satisfying message for us to deliver is that yes, there is enough. To that end, we must ensure clients stay within their plan at and throughout retirement. That means ongoing checkups to avoid the trap of spending too much, but also to ensure they spend enough (or at least the amount upon which our plan was based) to enjoy their lives.

I have had the great fortune of helping clients for nearly 28 years. It is so gratifying to receive notes or pictures from my clients showing how they have used their money to enrich their lives. Be that a dream home, a trip with family, a charitable donation, or helping send that child or grandchild to college, the “Abundance” mindset that good financial planning can accomplish is what gets me up in the morning. Freedom is not always freedom from something; better stated, it is the freedom to do or be what you want. Here’s hoping retirement can lend a hand in creating that freedom.

Slightly grainy picture of a client’s view of Mount Everest from an airplane, taken January 2024.

Brian O’Neill, CFP® is a financial advisor in the Atlanta office of Cahaba Wealth Management, www.cahabawealth.com.

Cahaba Wealth Management is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by the SEC nor does it indicate that the adviser has attained a particular level of skill or ability. Cahaba Wealth Management is not engaged in the practice of law or accounting. Always consult an attorney or tax professional regarding your specific legal or tax situation. Content should not be construed as personalized investment advice. The opinions in this materials are for general information, and not intended to provide specific investment advice or recommendations for an individual. Content should not be regarded as a complete analysis of the subjects discussed. To determine which investment(s) may be appropriate for you, consult your financial advisor.