Insights & Perspectives from Financial Advisors Near You

Stay informed with timely commentary, thoughtful analysis, and real-world financial insights from the team at Cahaba Wealth Management. Our blog and podcast offer a deeper look into the trends, strategies, and market developments shaping today’s financial landscape. Whether you’re looking to better understand investment principles, navigate economic shifts, or explore planning strategies for your future, we are here to help you make more confident, informed decisions.

This November, we’re proud to celebrate 16 years of helping clients live with clarity and confidence in their financial lives.

From day one, our mission has been simple and steadfast: to serve as trusted partners in guiding thoughtful, values-based financial decisions through customized financial planning and investment management. Sixteen years later, that mission continues to drive everything we do — and as of December 31, 2024, we’re honored to manage over $1.6 billion in client assets.

At Cahaba Wealth Management, we believe our success begins and ends with people. Relationships are at the core of our culture: valuing the person first, communicating with empathy, and fostering teamwork, balance, and a sense of community in all we do.

We’re deeply grateful for our incredible team, whose dedication and heart make Cahaba what it is — and for our clients, who trust us to walk alongside them through each chapter of life.

Here’s to continued growth and many more years doing what we love!

Cahaba Wealth Management is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by the SEC nor does it indicate that the adviser has attained a particular level of skill or ability. Cahaba Wealth Management is not engaged in the practice of law or accounting. Always consult an attorney or tax professional regarding your specific legal or tax situation. Content should not be construed as personalized investment advice. The opinions in this materials are for general information, and not intended to provide specific investment advice or recommendations for an individual. Content should not be regarded as a complete analysis of the subjects discussed. To determine which investment(s) may be appropriate for you, consult your financial advisor.

By now, we assume all Cahaba Wealth clients know that we do not react to short-term movements in the stock market. As we’ve said time and again, market volatility is a constant that allows stocks to generate higher returns than safer investments like cash and bonds. Successful long-term investment is difficult because it requires discipline. Short-term pullbacks are frequently accompanied by narratives that only serve to reinforce the accompanied anxiety. Telling yourself to remain calm and not react during these periods is what separates the opportunities from setbacks.

We were not surprised that President Trump announced tariffs on Wednesday. What was a surprise was the breadth of the sweeping tariffs. This subsequently caused panic and the resulting selloff in stocks. At the close of Friday’s trading, the S&P 500 was down nearly 10% in the last two days, and the S&P 600 (US small company stocks) lost almost 12% in that span. Selling has been indiscriminate and has spread to stocks around the world. We are not ones to react with panic to this kind of movement, but we certainly feel the need to comment on this climate.

As many of our long-term clients know, we have lived through several bizarre scenarios over the past 30 years. Between the 2000-2002 dot.com bubble bursting, the financial crisis of 2008-2009, Covid, and the bond bear market of 2022, it’s been a whirlwind. During these phases, we have used financial planning and cash flow projections to help our clients navigate these various challenges. In most cases, they continue to thrive and achieve financial goals. Even with those specific market downturns, portfolios continue to be positive over that timeframe, and investing remains the best option to outstrip inflation and grow assets. That perspective hasn’t changed with the recent announcements.

Perhaps one positive of this week is the return of bonds to the “safety” trade. US bonds are up roughly 1% this week, over 3.5% year to date, and are providing the cushion that a balanced portfolio should hope for during stock downturns. Diversification works! With the 10-Year Treasury at or below 4%, we may also see a decrease in Federal interest payments and the possibility to refinance recent mortgages.

The stated goal of the tariff strategy is to bring more balance to the global trade landscape and improve US national security. Both goals are logical and appear to be in the best long-term interest of the United States. However, achieving these goals is complicated. Onshoring manufacturing and negotiating reciprocal trade agreements does not happen overnight. In addition, the near-term impact of tariffs is perceived by economists as an immediate tax. The desire to have the United States economy increase the percentage of GDP generated through manufacturing is achievable but will need to be navigated carefully to avoid major economic disruption.

The unpredictable nature of how the tariff strategy was announced is causing the markets the most consternation. One thing that markets hate is uncertainty. Is The President simply using this as a negotiating tactic with each country to get a better deal? How long will these tariffs be in place? Will the tariffs end up either receding or going away altogether? We currently don’t know the answer to any of these questions. What we do know is that once clarity returns, stocks will rejoice.

We hold our convictions that planning and long-term views of cash flow allow clients to weather any storm. Your asset allocation is designed for this very situation. Where possible, we will explore opportunities to use this downturn to our clients’ long-term advantage. If you feel more anxiety and concern about your portfolio than you normally might, it may be a sign that your risk tolerance is not in line with your asset allocation. Please reach out if you would like to discuss in greater detail. In the meantime, we are confident that this pullback will join the previous selloffs as a long-term buying opportunity.

As always, thank you for your trust and confidence.

Cahaba Wealth Management is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by the SEC nor does it indicate that the adviser has attained a particular level of skill or ability. Cahaba Wealth Management is not engaged in the practice of law or accounting. Always consult an attorney or tax professional regarding your specific legal or tax situation. Content should not be construed as personalized investment advice. The opinions in this materials are for general information, and not intended to provide specific investment advice or recommendations for an individual. Content should not be regarded as a complete analysis of the subjects discussed. To determine which investment(s) may be appropriate for you, consult your financial advisor.

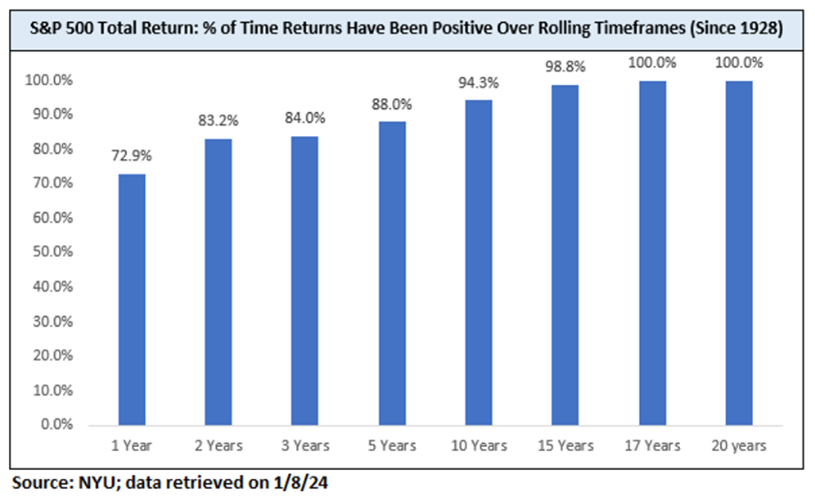

“Should I invest now (or stay invested) if the stock market is at all-time highs?” Given there are so many all-time highs in the stock market, we are asked to answer this question with shocking frequency. We know that over time the market goes up, but there tends to be more emphasis and concern about the timing of the next drop or bear market. It is enticing to think we can manage our portfolios to avoid such situations. In reality, if an investment’s time horizon was long enough, the stock market has ALWAYS provided positive returns. So, how long is “long enough”?

Since 1928, S&P 500 returns have been positive over a one-year period 73% of the time1. Not a bad percentage! If you have a ten year investment time horizon, which most of our clients do, the stock market has produced a positive return in 94% of those ten-year periods. When we extend the time horizon to twenty years, we see that returns have been positive 100% of the time. Although past performance is not indicative of future results, historical data shows that staying invested through market turbulence has always been the better decision.

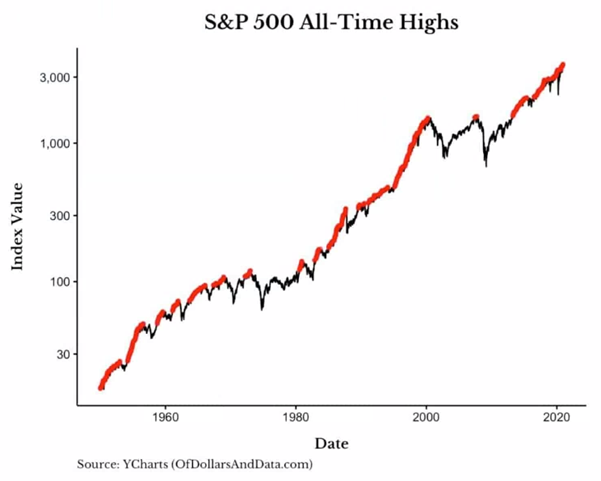

Conversely, what happens when the market is at all-time highs? Let’s first look at a chart depicting S&P 500 returns since the 1950s:

Each red instance on the accompanying chart represents days when the stock market reached an all-time high. As expected, this chart does have periods where the market did not reach its peak (i.e., returns represented by a black line), but there are more red sections than there are not. One of the most interesting components of the chart is that the red portions tend to bunch together. In other words, all-time highs have historically signaled more all-time highs. While different analysts and economists often debate the market and its parameters, the data supports this general concept in almost every case!

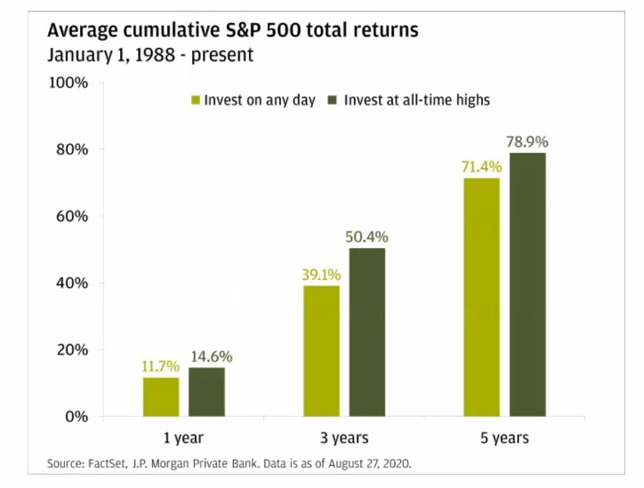

The following table pulls from a 1988-2020 dataset of market returns and supports the claim that investing during all-time highs has not been detrimental to investors. Over this time period, the average one year return in the stock market following an all-time high was 14.6%, beating the average return from investing on any given day throughout the data sample. Cumulatively, over the next five years following an all-time high in the market, an investor’s portfolio would have done materially better by investing at an all-time high as opposed to picking any other starting day at random (78.9% vs 71.4%).

The data – despite its source or time frame – generally comes to the same conclusion: one is better investing at all-time highs than they are by picking a day at random to invest. There is a consensus throughout financial research that this benefit has the greatest impact for time periods in the 1-5 year range. Said differently, as your investment horizon extends, timing takes a back seat to consistency when considering the long-term benefit. In the long run, the market goes up and investors are compensated time and time again for the risk they are taking.

By knowing your risk tolerance and your investment horizon (the time you have until you need to access your money), you can invest intelligently and improve your specific long-term outcomes. We encourage portfolio diversification and client-specific market risk exposure. This is why we prioritize knowing clients’ parameters and risk tolerances here at Cahaba Wealth.

Arguably the greatest caveat to our discussion is that no one can successfully and consistently time the market over the long run. This has been proven time and time again! Pretending to know which all-time high is the last one for the foreseeable future is nearly impossible. Stay away from this trap. Be diversified, take the appropriate amount of market risk and stay invested!

Don Keeney, CFA, CFP® is a financial advisor in the Nashville office of Cahaba Wealth Management, www.cahabawealth.com.

Cahaba Wealth Management is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by the SEC nor does it indicate that the adviser has attained a particular level of skill or ability. Cahaba Wealth Management is not engaged in the practice of law or accounting. Always consult an attorney or tax professional regarding your specific legal or tax situation. Content should not be construed as personalized investment advice. The opinions in this materials are for general information, and not intended to provide specific investment advice or recommendations for an individual. Content should not be regarded as a complete analysis of the subjects discussed. To determine which investment(s) may be appropriate for you, consult your financial advisor.